Predictive modeling involves predicting a variable of interest relating to an observation, based upon other attributes we know about that observation.

One approach to doing so is to start by specifying the structure of the model with certain numeric parameters left unspecified. These ‘unspecified parameters’ are then calculated in a way as to fit the available data as closely as possible. This general approach is called parametric modeling.

There are other approaches as well, for example with decision trees we find ever more ‘pure’ subsets by partitioning data based on the independent variables.

Linear regression belongs to the former category, ie, we specify a general model (\(y = \alpha + \beta_1 x_1 + \beta_2 x_2 + ... + \epsilon\)) and calculate the parameters (the coefficients).

The linear model assumes that the relations between variables can be summarized by a straight line.

Linear regression is used extensively in industry, finance and practically all forms of research. A huge advantage of regression models is their explainability as we can see the equations used to predict the target variable.

Univariate Regression

Regression with a single dependent variable y whose value is dependent upon the independent variable x is expressed as \(y = \alpha + \beta x + \epsilon\) where \(\alpha\) is a constant, so is \(\beta\). \(x\) is the independent variable and \(\epsilon\) is the error term (more on the error term later).

Given a set of data points, it is fairly easy to calculate alpha and beta – and while it can be done manually, it can be also be done using Excel using the SLOPE (for calculating β) and the INTERCEPT (α) functions.

If done manually, beta is calculated as:

> \(\beta\) = covariance of the two variables / variance of the independent variable

Once beta is known, alpha can be calculated as

> \(\alpha\) = mean of the dependent variable (ie \(y\)) - \(\beta\) * mean of the independent variable (ie \(x\))

Predictions

Once \(\alpha\) and \(\beta\) are known, it is probably possible to say that we can ‘predict’ \(y\) if we know the value of \(x\).

The ‘predicted’ value of \(y\) is provided to us by the regression equation. This is unlikely to be exactly equal to the actual observed value of \(y\).

The difference between the two is explained by the error term - \(\epsilon\). This is a random ‘error’ – error not in the sense of being a mistake – but in the sense that the value predicted by the regression equation is not equal to the actual observed value.

An Example

Instead of spending more time on the theory behind regression, let us jump right into an example. We have the mpg datset where we know the miles-per-gallon for a set of cars, and also other attributes related to the car such as the number of cylinders, engine size (displacement) etc.

We can try to set up a regression model where we attempt to predict the miles-per-gallon (mpg) from the rest of the columns in the dataset.

Usual library imports first

Code

import numpy as npimport matplotlib.pyplot as pltimport pandas as pdimport statsmodels.api as smimport seaborn as snsfrom scipy import statsfrom sklearn import datasetsfrom sklearn import metricsfrom sklearn.preprocessing import PolynomialFeaturesfrom sklearn.metrics import mean_squared_errorimport sklearn.preprocessing as preprocimport statsmodels.formula.api as smffrom sklearn.metrics import confusion_matrix, accuracy_score, classification_report, ConfusionMatrixDisplayfrom sklearn.metrics import mean_absolute_error, mean_squared_errorfrom sklearn.model_selection import train_test_split

13.1 OLS Regression

13.1.1 Load mtcars dataset

Consider the mtcars dataset. It has data for 32 cars, 11 variables for each.

mpg

Miles/(US) gallon

cyl

Number of cylinders

disp

Displacement (cu.in.)

hp

Gross horsepower

drat

Rear axle ratio

wt

Weight (1000 lbs)

qsec

1/4 mile time

vs

Engine (0 = V-shaped, 1 = straight)

am

Transmission (0 = auto, 1 = manual)

gear

Number of forward gears

Can we calculate miles-per-gallon (mpg) for a car based on the other variables?

Code

# Let us load the data and look at some sample columnsmtcars = sm.datasets.get_rdataset('mtcars').datamtcars.sample(4)

13.1.2 Split dataset between X (features, or predictors) and y (target)

The mpg column contains the target, or the y variable. This is the first column in our dataset. The rest of the variables will be used as predictors, or the X variables.

We want to create a model with an intercept. In Statsmodels, that requires us to use the function add_constant as shown below.

Code

y = mtcars.mpg.values# sm.add_constant adds a column to the dataframe with 1.0 as a constantfeatures = mtcars.iloc[:,1:]X = sm.add_constant(features)

# Let us check if the shape of the different dataframes is what we would expect them to beprint('Shape of the original mtcars dataset (rows x columns):', mtcars.shape)print('Shape of the X dataframe, has a new col for constant (rows x columns):', X.shape)print('Shape of the features dataframe (rows x columns):', features.shape)

Shape of the original mtcars dataset (rows x columns): (32, 11)

Shape of the X dataframe, has a new col for constant (rows x columns): (32, 11)

Shape of the features dataframe (rows x columns): (32, 10)

13.1.3 Build model and obtain summary

Code

# Now that we have defined X and y, we can easily fit a regression model to this datamodel = sm.OLS(y, X).fit()model.summary()

OLS Regression Results

Dep. Variable:

y

R-squared:

0.869

Model:

OLS

Adj. R-squared:

0.807

Method:

Least Squares

F-statistic:

13.93

Date:

Sat, 02 Mar 2024

Prob (F-statistic):

3.79e-07

Time:

11:22:20

Log-Likelihood:

-69.855

No. Observations:

32

AIC:

161.7

Df Residuals:

21

BIC:

177.8

Df Model:

10

Covariance Type:

nonrobust

coef

std err

t

P>|t|

[0.025

0.975]

const

12.3034

18.718

0.657

0.518

-26.623

51.229

cyl

-0.1114

1.045

-0.107

0.916

-2.285

2.062

disp

0.0133

0.018

0.747

0.463

-0.024

0.050

hp

-0.0215

0.022

-0.987

0.335

-0.067

0.024

drat

0.7871

1.635

0.481

0.635

-2.614

4.188

wt

-3.7153

1.894

-1.961

0.063

-7.655

0.224

qsec

0.8210

0.731

1.123

0.274

-0.699

2.341

vs

0.3178

2.105

0.151

0.881

-4.059

4.694

am

2.5202

2.057

1.225

0.234

-1.757

6.797

gear

0.6554

1.493

0.439

0.665

-2.450

3.761

carb

-0.1994

0.829

-0.241

0.812

-1.923

1.524

Omnibus:

1.907

Durbin-Watson:

1.861

Prob(Omnibus):

0.385

Jarque-Bera (JB):

1.747

Skew:

0.521

Prob(JB):

0.418

Kurtosis:

2.526

Cond. No.

1.22e+04

Notes: [1] Standard Errors assume that the covariance matrix of the errors is correctly specified. [2] The condition number is large, 1.22e+04. This might indicate that there are strong multicollinearity or other numerical problems.

At this point, the model itself is contained in an object called model.

A useful function for the t-distribution is the t function available from scipy. t.cdf gives us the area under the curve from -∞ to the value of x provided, ie it gives area under the curve (-∞, x].

The distance from 0 in terms of multiples of standard deviation tells you how far the coefficient is from zero. The farther it is, the likelier that its value is not a fluke, and it is indeed different from zero.

So the right tail is the area under the curve, but you have to multiply that by two as you need to see the area under the curve on both sides of zero.

Code

# for the 'cyl' coefficient above, the t value is (or distance from zero in terms of SD) is -0.107from scipy.stats import t t.cdf(x =-0.107, df =21) *2

0.9158046158959711

13.1.4 Use Model to Perform Predictions

Once the model is created, creating predictions is easy. We do so with the predict method on the model object we just created. In fact, this is the way we will be doing predictions for all models, not just regression.

Code

model.predict(X)

rownames

Mazda RX4 22.599506

Mazda RX4 Wag 22.111886

Datsun 710 26.250644

Hornet 4 Drive 21.237405

Hornet Sportabout 17.693434

Valiant 20.383039

Duster 360 14.386256

Merc 240D 22.496012

Merc 230 24.419090

Merc 280 18.699030

Merc 280C 19.191654

Merc 450SE 14.172162

Merc 450SL 15.599574

Merc 450SLC 15.742225

Cadillac Fleetwood 12.034013

Lincoln Continental 10.936438

Chrysler Imperial 10.493629

Fiat 128 27.772906

Honda Civic 29.896739

Toyota Corolla 29.512369

Toyota Corona 23.643103

Dodge Challenger 16.943053

AMC Javelin 17.732181

Camaro Z28 13.306022

Pontiac Firebird 16.691679

Fiat X1-9 28.293469

Porsche 914-2 26.152954

Lotus Europa 27.636273

Ford Pantera L 18.870041

Ferrari Dino 19.693828

Maserati Bora 13.941118

Volvo 142E 24.368268

dtype: float64

Code

# Let us look at what the model object prints as.# It is really a black boxmodel

<statsmodels.regression.linear_model.RegressionResultsWrapper at 0x1d059169910>

But how do we know this model is any good?

Intuition tells us that the model will be good if its predictions are close to what the actual observations are. So we can calculate the predicted values of mpg, and compare them to the actual values.

Let us do that next - we compare the actual mpg to predicted mpg.

count 32.000

mean 0.000

std 2.181

min -3.451

25% -1.604

50% -0.120

75% 1.219

max 4.627

Name: difference, dtype: float64

13.2 Assessing the regression model

Next let us look at some formal methods of assessing regression

13.2.1 Standard Error of Regression

Conceptually, the standard error of regression is the same as the standard deviation we calculated above from the differences between actual and predicted values. However, it is not mathematically pure and we have to consider the degrees of freedom to get the actual value, which we call the standard error of regression.

The standard error of regression takes into account the degrees of freedom lost due to the number of regressors in the model, and the number of observations the model is based on. It it considered a more accurate representation of the standard error of regression than the crude standard deviation calculation we did earlier.

Code

# Calculated as:model.mse_resid**.5

2.650197027865509

Code

# Also as:np.sqrt(np.sum(model.resid**2)/model.df_resid)

2.650197027865509

Code

# Also calculated directly from the model asmodel.scale**.5

2.650197027865509

model.resid is the residuals, and model.df_resid is the degrees of freedom for the model residuals

Code

print(model.resid)print('\nCount of items above = ', len(model.resid))

rownames

Mazda RX4 -1.599506

Mazda RX4 Wag -1.111886

Datsun 710 -3.450644

Hornet 4 Drive 0.162595

Hornet Sportabout 1.006566

Valiant -2.283039

Duster 360 -0.086256

Merc 240D 1.903988

Merc 230 -1.619090

Merc 280 0.500970

Merc 280C -1.391654

Merc 450SE 2.227838

Merc 450SL 1.700426

Merc 450SLC -0.542225

Cadillac Fleetwood -1.634013

Lincoln Continental -0.536438

Chrysler Imperial 4.206371

Fiat 128 4.627094

Honda Civic 0.503261

Toyota Corolla 4.387631

Toyota Corona -2.143103

Dodge Challenger -1.443053

AMC Javelin -2.532181

Camaro Z28 -0.006022

Pontiac Firebird 2.508321

Fiat X1-9 -0.993469

Porsche 914-2 -0.152954

Lotus Europa 2.763727

Ford Pantera L -3.070041

Ferrari Dino 0.006172

Maserati Bora 1.058882

Volvo 142E -2.968268

dtype: float64

Count of items above = 32

Code

model.df_resid

21.0

13.2.2 Goodness of fit, R-squared

R-squared is the square of the correlation betweeen actual and predicted values

Intuitively, we would also like to see a high correlation between predictions and observed values. We have the predicted and observed values, so calculating the R-squared is easy. (R-squared is also called coefficient of determination.)

Code

# Calculate the correlations between actual and predictedround(compare.corr(), 6)

mpg

pred

difference

mpg

1.000000

0.93221

0.361917

pred

0.932210

1.00000

-0.000000

difference

0.361917

-0.00000

1.000000

Code

# Squaring the correlations gives us the R-squared round(compare.corr()**2, 6)

mpg

pred

difference

mpg

1.000000

0.869016

0.130984

pred

0.869016

1.000000

0.000000

difference

0.130984

0.000000

1.000000

Code

# Why did we use the function `round` above?# To avoid the scientific notation and make the # results easier to read. For example, without# using the rounding we get the below result.compare.corr()**2

mpg

pred

difference

mpg

1.000000

8.690158e-01

1.309842e-01

pred

0.869016

1.000000e+00

2.538254e-27

difference

0.130984

2.538254e-27

1.000000e+00

13.2.3 Root mean squared error

The RMSE is just the square root of the average squared errors. It is the same as if we had calculated the population standard deviation based on the residuals.

RMSE is normally calculated for the test set, because for the training data we have the standard error of regression.

Let us calculate it here for the entire dataset as we did not do a train-test split for this example.

This is the average difference between the actual and the predicted values, ignoring the sign of the difference.

More Robust Evaluation: K-Fold Cross-Validation. A single train-test split can give optimistic or pessimistic results depending on the random seed. K-fold CV gives a more reliable estimate by training and evaluating on K different splits:

from sklearn.model_selection import cross_val_score, KFoldfrom sklearn.linear_model import LinearRegressionmodel_cv = LinearRegression()kf = KFold(n_splits=5, shuffle=True, random_state=42)# cross_val_score returns negative MSE by convention; negate to get positive RMSErmse_scores = (-cross_val_score(model_cv, X, y, cv=kf, scoring="neg_mean_squared_error")) **0.5print(f"RMSE: {rmse_scores.mean():.2f} +/- {rmse_scores.std():.2f}")

Code

mean_absolute_error(compare.pred, compare.mpg)

1.7227401628911079

13.2.5 Understanding the F-statistic, and its p-value

The R-squared is a key statistic for evaluating regression. But it is also a statistical quantity, which means it is an estimate around which exists a confidence interval.

Estimates follow distributions, and often we see statements such as a particular variable follows the normal or lognormal distribution. The value of R2 follows what is called an F-distribution.

The F-distribution has two parameters – the degrees of freedom for each of the two variables ESS and TSS that have gone into calculating R2. The F-distribution has a minimum of zero, and approaches zero to the right of the distribution. In order to test the significance of R2, one needs to calculate the F statistic. Then we need to find out how likely is that value of the F-stat to have been obtained by chance – lower this likelihood, the better it is.

The question arises as to how ‘significant’ is any given value of R2? Could this have been zero, and we just happened randomly to get a value of 0.86?

The F-test of overall significance is the hypothesis test for this relationship. If the overall F-test is significant, you can conclude that R-squared does not equal zero, and the correlation between the model and dependent variable is statistically significant.

To do this test, we calculate the F statistic, and its p-value. If the p-value is less than our desired level of significance (say, 5%, or 95% confidence level), then we believe the value was not arrived at by chance. This is the standard hypothesis testing piece.

\(\mbox{F-stat} = \frac{\frac{\mbox{Explained sum of squares}}{\mbox{Degrees of Freedom of the model}}}{\frac{\mbox{Residual sum of squares}}{\mbox{Degrees of Freedom fo the Residuals}}}\)

Fortunately, the F-stat, and its p-value can be easily obtained in Python, and we do not need to worry about calculations.

Code

# F stat= (explained variance) / (unexplained variance)# F stat = (ESS/DFM) / (RSS/DFE)(model.ess/model.df_model) / (np.sum(model.resid**2)/model.df_resid)

13.932463690208827

Code

# p value for F statimport scipy1-(scipy.stats.f.cdf(model.fvalue, model.df_model, model.df_resid))

3.7931521057466e-07

Code

# Getting f value directly from statsmodelsmodel.fvalue

13.932463690208827

Code

# Getting the p value of the f statistic directly from statsmodelsmodel.f_pvalue

3.7931521053058665e-07

Code

# Source: http://facweb.cs.depaul.edu/sjost/csc423/documents/f-test-reg.htm# Degrees of Freedom for Model, p-1, where p is number of regressors dfm = model.df_modeldfm

10.0

Code

# n-p, Deg Fdm for Errors, where n is number of observations, and p is number of regressorsmodel.df_resid

21.0

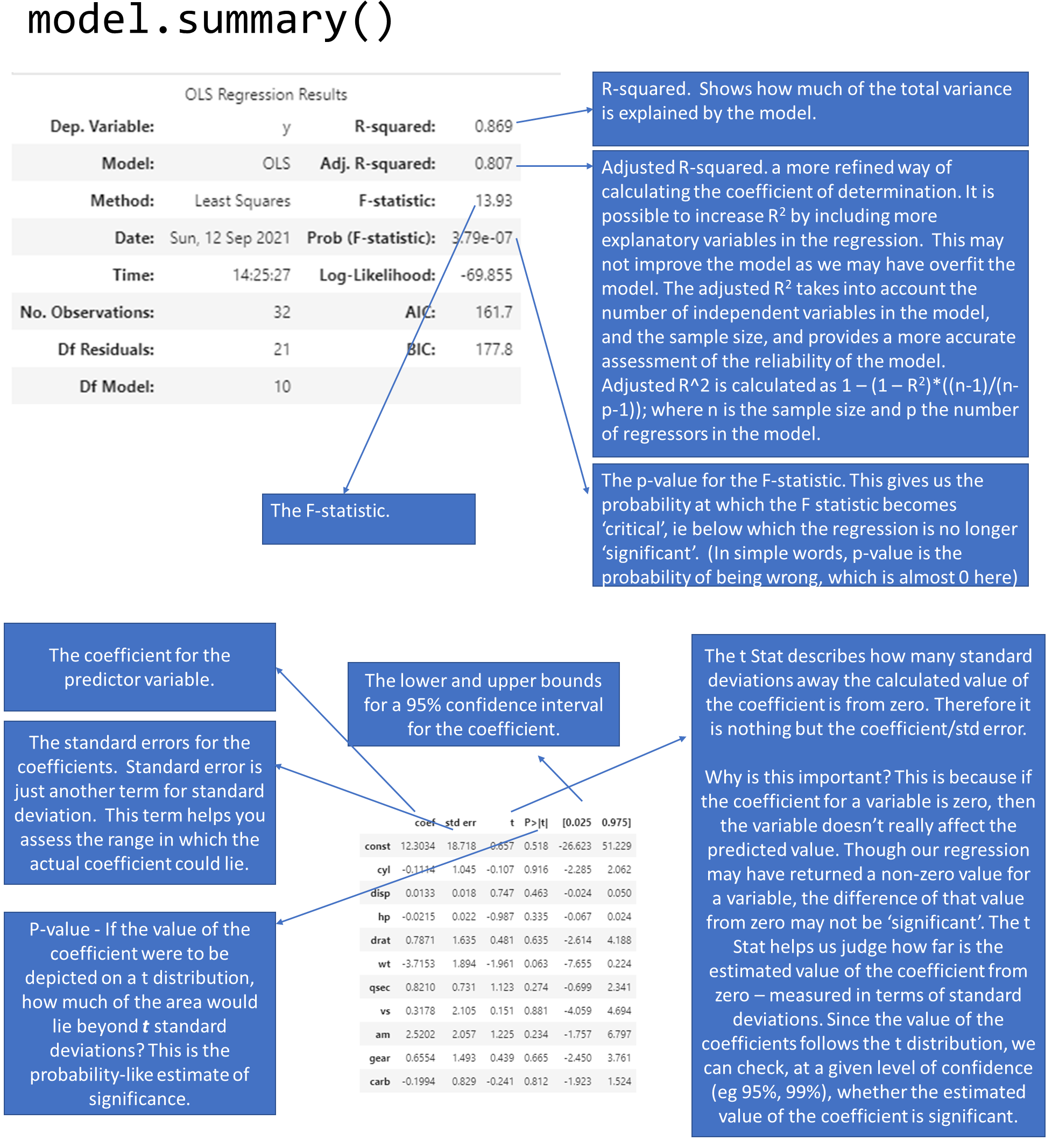

13.2.6 Understanding the model summary

With what we now know about R-squared, the F-statistic, and the coefficients, we can revisit our model summary that statsmodels produced for us. The below graphic explains how to read the model summary.

image.png

Significance of the Model vs Significance of the Coefficients

The model’s overall significance is judged by the value of the F-statistic.

Each individual coefficient also has a p-value, meaning individual coefficients may be statistically insignificant.

It is possible that the overall regression is significant, but none of the coefficients are. These cases can be caused by multi-collinearity, but it does not prevent us from using the predictions from the model. However it does limit our ability to definitively say which variables are the most important for our model.

If the reverse situation is true, ie the model isn’t significant but some of the variables have statistically significant coefficients, we can’t use the model.

If multi-collinearity needs to be addressed, we can do so by combining the independent variables that are correlated, eg using PCA.

For our goals of prediction in business, we are often more interested in being roughly right (and get a ‘lift’) than statistical elegance.

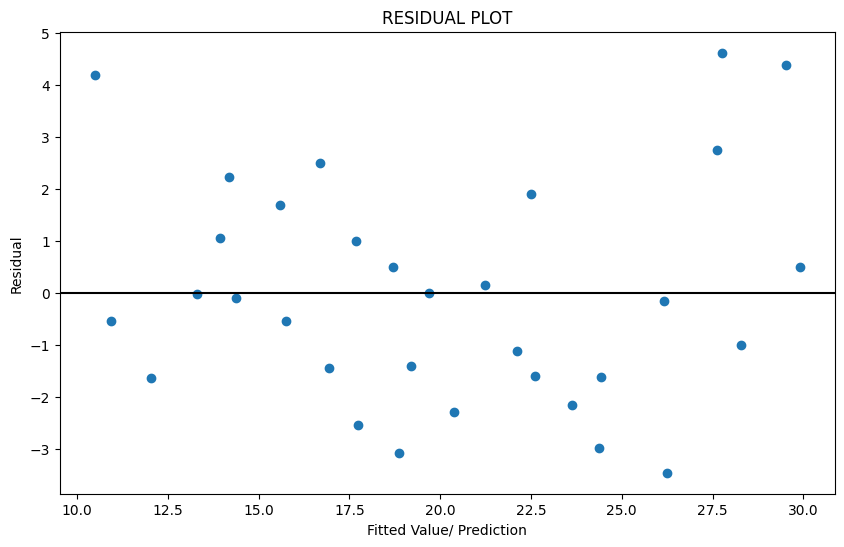

13.2.7 Plot the Residuals

We mentioned that the residuals, or our \(\epsilon\) term, are unexplained by the data. Which means they should not show any pattern, and should appear to be completely random. This is because any pattern should have been captured by our regression model and not show up in the residuals.

Sometimes we do see a pattern because of the way our data is, and we want to make sure that is not the case.

To check, the first thing we do is to plot the residuals. We should not be able to discern any obvious pattern in the plot. Which does not appear to be the case here.

Often when we notice a non-random pattern, this is due to heteroscedasticity (which means that the variance of the feature set is not constant). If we do notice heteroscedasticity, we may have to transform the inputs to get constant variance (eg, a logarithmic transform, or a Box-Cox transform).

The residual plot is a scatterplot of the residuals vs the fitted value (prediction). See the graphic above plotting the residuals for our miles-per-gallon model. Do you think the residuals are randomly distributed?

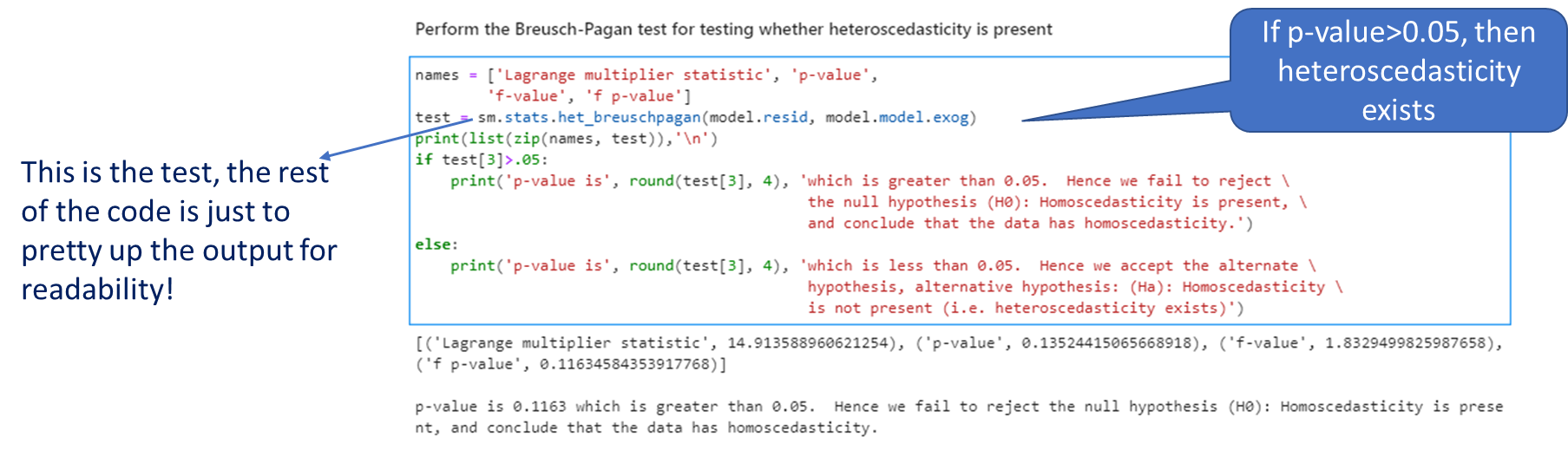

13.2.8 Test for Heteroscedasticity - Breusch-Pagan test

OLS regression assumes that the data comes from a population with constant variance, or homoscedasticity.

However, often that is not the case. This situation is called heteroscedasticity. This reflects itself in a pattern visible on the residual plot.

The problem with heteroscedasticity is that the confidence intervals for the regression coefficients may be understated. Which means we may consider something to be significant, when it is not.

We can address heteroscedasticity by transforming the variables (eg using the Box-Cox transformation, which is covered later in feature engineering). As a practical matter, heteroscedasticity may be difficult to identify visually from a residual plot, so we use a test for that.

The Breusch-Pagan test for heteroscedasticity is a test of hypothesis that compares two hypothesis:

H-0: Homoscedasticity is present.

H-alt: Homoscedasticity is not present.

Fortunately for us, we do not need to think too hard about the math as this is implemented for us in a function in statsmodels. The function requires two variables as inputs: model residuals, and model inputs. Once you have already created a model, these two are easy to get using model attributes.

If the p-value from the function is greater than our desired confidence, we conclude that the data has homoscedasticity.

Interpreting the test

image.png

Code

names = ['Lagrange multiplier statistic', 'p-value','f-value', 'f p-value']test = sm.stats.het_breuschpagan(model.resid, model.model.exog)print(list(zip(names, test)),'\n')if test[3]>.05:print('p-value is', round(test[3], 4), 'which is greater than 0.05. Hence we fail to reject \ the null hypothesis (H0): Homoscedasticity is present, \ and conclude that the data has homoscedasticity.')else:print('p-value is', round(test[3], 4), 'which is less than 0.05. Hence we accept the alternate \ hypothesis, alternative hypothesis: (Ha): Homoscedasticity \ is not present (i.e. heteroscedasticity exists)')

[('Lagrange multiplier statistic', 14.913588960622171), ('p-value', 0.13524415065665535), ('f-value', 1.8329499825989772), ('f p-value', 0.1163458435391346)]

p-value is 0.1163 which is greater than 0.05. Hence we fail to reject the null hypothesis (H0): Homoscedasticity is present, and conclude that the data has homoscedasticity.

13.2.9 Summarizing

To assess the quality of a regression model, look for the following: 1. The estimate of the standard error of the regression. Check how large the number is compared to the mean of the observed variable.

2. The R-squared. The closer the value of R-square is to 1, the better it is. (R-square will be a number between 0 and 1). It tells you how much of the total variance in the target variable is explained by the regression model.

3. Check for the significance of the R-squared by looking at the p-value for the F-statistic. This is a probability-like number that estimates how likely is it to have obtained the R-square value by random chance. The lower this is, the better.

4. Examine the coefficients for each of the predictor variables. Also look at the p-values for the predictors to see if they are significant.

5. Finally, have a look at a plot of the residuals.

Residual Diagnostics Quick Reference. A well-specified regression model should produce residuals that are: (1) centered around zero with no systematic bias, (2) roughly normally distributed (check with a Q-Q plot), and (3) homoscedastic — constant variance across fitted values (check with residuals vs. fitted plot). Non-random residual patterns signal a missing feature, a non-linear relationship, or a mis-specified model. Corrective actions: add interaction terms, apply a log-transform, or switch to a non-parametric approach.

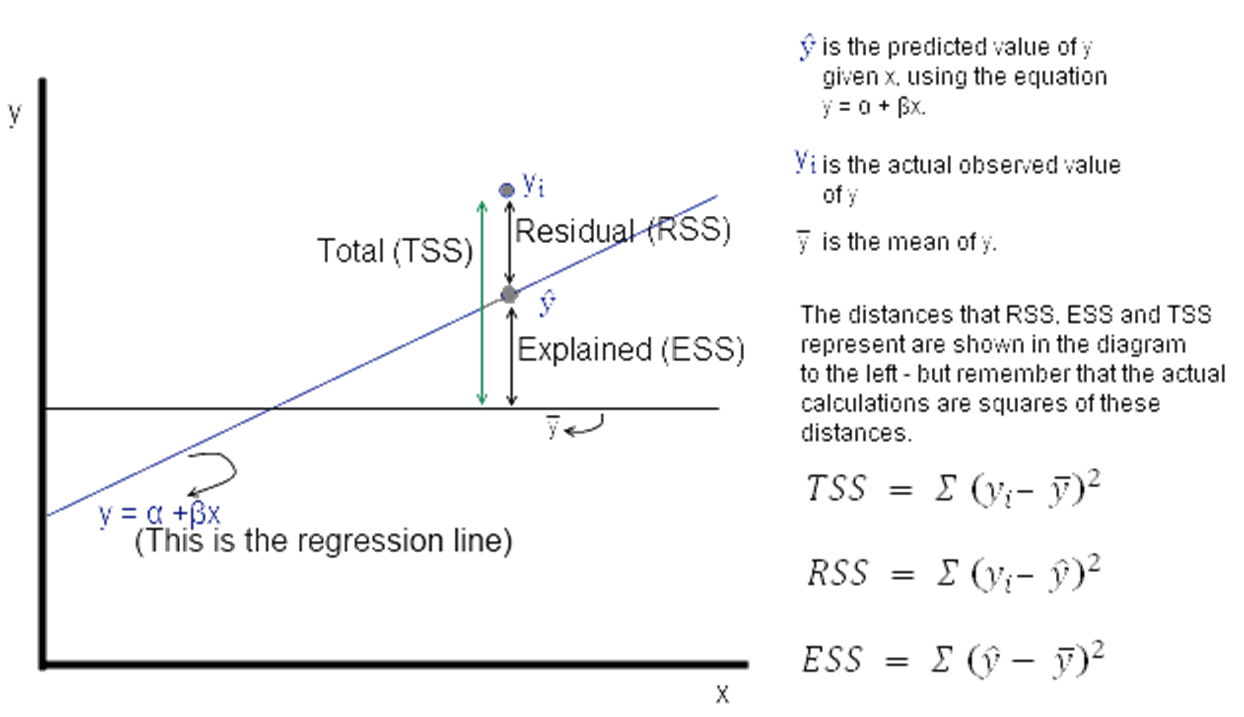

13.2.10 Understanding Sums of Squares

ESS, TSS and RSS calculations

\(y_i\) is the actual observed value of the dependent variable, \(\hat{y}\) is the value of the dependent variable according to the regression line, as predicted by our regression model. What we want to get is a feel for is the variability of actual \(y\) around the regression line, ie, the volatility of \(\epsilon\). This is given by the distance \(y_i\) minus \(\hat{y}\). Represented in the figure as RSS.

image.png

Now \(\epsilon\) = observed – expected value of \(y\)

Thus, \(\epsilon = y_i - \hat{y}\). The sum of \(\epsilon\) is expected to be zero. So we look at the sum of squares:

The value of interest to us is \(= \sum {(y_i - \hat{y})^2}\). Since this value will change as the number of observations change, we divide by ‘n’ to get a ‘per observation’ number. (Since this is a square, we take the root to get a more intuitive number, ie the RMS error explained a little while earlier. Effectively, RMS gives us the standard deviation of the variation of the actual values of y when compared to the observed values.)

If \(s\) is the standard error of the regression, then \(s = \sqrt{RSS/(n – 2)}\)

(where \(n\) is the number of observations, and we subtract 2 from this to take away 2 degrees of freedom.)

0.8690157644777646

RSS 147.4944300166507

ESS 978.5527574833491

TSS 1126.0471874999998

ESS+RSS= 1126.0471874999998

F value 199.03519557441183

ESS/TSS= 0.8690157644777646

13.3 Lasso and Ridge Regression

Introduction

The setup:

We saw multinomial regression expressed as: \(y = \beta_0 + \beta_1 + \beta_2 + ... + \epsilon\)

We can combine all the \(x_n\) variables into a single array, and call it \(X\). Similarly, we can combine the \(\beta_n\) coefficients into another vector called \(\beta\).

Then the regression equation can be expressed as \(y = X\beta + \epsilon\), which is a more succinct form.

Regularization

Regularization means adding a penalty to our objective function with a view to reducing complexity. Complexity may appear in the form of:

- the number of variables in a model, and/or

- the value of the coefficients.

Why is complexity bad in models?

One reason: overfitting. Complex models tend to fit well to training data, and do not generalize well.

Another challenge with complexity in OLS regression is that the value of \(\beta\) is very sensitive to changes in X. What that means is adding a few new observations, or taking out a few can dramatically change the value of the coefficients in our vector \(\beta\).

This is because OLS will often determine coefficient values to be large numerical quantities that can fluctuate by large margins if the inputs change. So:

You have a less stable model, and

Your model likely suffers from overfitting

We address this problem by adding a penalty for coefficient values.

Modifying the objective function

In an OLS model, our objective function aims to minimize the sum of squares of the residuals. It doesn’t care about how many variables it includes in the model (a variable is considered included in a model if it has a non-zero coefficient), or what the values of the coefficients are.

But we can change our objective function to force it to consider our goals of reducing the weights. We do this by adding to our objective function a cost that is related to the values of the weights. Problem solved!

Current Objective Function: Minimize Least Squares of the Residuals

Types of regularization

Two types of regularization:

- L1 regularization—The cost added is dependent on the absolute value of the weight coefficients (the L1 norm of the weights).

- L1 norm for a vector = sum of all elements

New Objective Function = Minimize (Least Squares of the Residuals + L1_wt L1 norm for the coefficients vector)* When L1 regularization is applied, we call it Lasso Regression

L2 regularization—The cost added is dependent on the square of the value of the weight coefficients (the L2 norm of the weights).

L2 norm for a vector = sqrt of the sum of squares of all elements

New Objective Function = Minimize (Least Squares of the Residuals + \(\alpha \cdot\) L2 norm for the coefficients vector)

When L2 regularization is applied, we call it Ridge Regression

ElasticNet: Best of Both. ElasticNet combines L1 and L2 penalties and is often the best default choice when you are unsure whether sparsity (Lasso) or coefficient shrinkage (Ridge) is more appropriate:

from sklearn.linear_model import ElasticNet# alpha: overall regularization strength# l1_ratio: 0 = pure Ridge, 1 = pure Lasso, 0.5 = equal mixen = ElasticNet(alpha=0.1, l1_ratio=0.5)en.fit(X_train, y_train)

Confidence vs. Prediction Intervals. An important and often confused distinction: - Confidence interval: Range within which the mean of Y falls for a given X (uncertainty about the regression line itself) - Prediction interval: Range within which a new individual observation of Y falls (always wider — includes both uncertainty about the line and natural variability)

In statsmodels, both are available from model.get_prediction(X_new).summary_frame().

L1 and L2 norms are easily calculated using the norm function in numpy.linalg.

How to calculate L1 norm manually

Code

np.linalg.norm([2,3], 1)

5.0

Code

np.linalg.norm([-2,3], 1)

5.0

Code

# same as sum of all elements2+3

5

How to calculate L2 norm manually

Code

np.linalg.norm([2,3], 2)

3.605551275463989

Code

# same as the root of the sum of squares of the elementsnp.sqrt(2**2+3**2)

3.605551275463989

13.3.1 Lasso and Ridge regression Statsmodels

Fortunately, when doing lasso or ridge regression, we only need to specify the values of \(\alpha\) and L1_wt, and the system does the rest for us.

In the statsmodels implementation of Lasso and Ridge regression, the below function is minimized.

where RSS is the usual regression sum of squares, n is the sample size, and \(|∗|_1\) and \(|∗|_2\) are the L1 and L2 norms.

Alpha is the overall penalty weight. It can be any number (ie, not just between 0 and 1).

The L1_wt parameter decides between L1 and L2 regularization. Must be between 0 and 1 (inclusive). If 0, the fit is a ridge fit, if 1 it is a lasso fit. (Because 0 often causes a divide by 0 error, use something small like \(1e-8\).)

Example

Next, we look at an example. Here is a summary of how to use statsmodels for regularized (ridge/lasso) regression:

In statsmodels, you have to specify at least two parameters to run Lasso/Ridge regression:

alpha

L1_wt

Remember that the function minimized is \(0.5*RSS/n + alpha*((1-L1\_wt)*|params|_2^2/2 + L1\_wt*|params|_1)\)

Alpha needs to be a value different from zero

L1_wt should be a number between 0 and 1.

If L1_wt = 1, then you are doing Lasso/L1 regularization

If L1_wt = 0, then you are doing Ridge/L2 regularization (Note: in statsmodels, you can’t use L1_wt = 0, have to use a tiny non-zero number, eg 1e-8 instead)

Values between 0 and 1 weight the regularization between L1 and L2 penalties

You can run a grid-search to find the values of alpha and L1_wt that give you the best results. (Grid search means a brute force search through many parameter values.)

Notes: [1] Standard Errors assume that the covariance matrix of the errors is correctly specified. [2] The condition number is large, 1.22e+04. This might indicate that there are strong multicollinearity or other numerical problems.

Code

# Comparing coefficients between normal OLS and Regularized Regressionpd.DataFrame({'model': model.params, 'model_reg': model_reg.params})

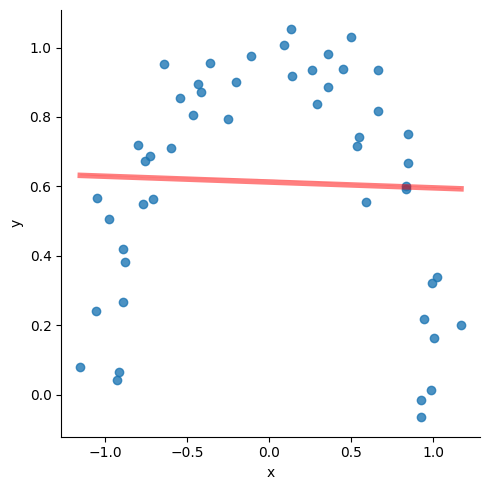

Consider the data below. The red line is the regression line with the following attributes:

> slope=-0.004549361971974567,

> intercept=0.6205433516646912,

> rvalue=-0.009903930817224469,

> pvalue=0.9455773121019574

Clearly, not a very good fit.

But it is pretty obvious that if the line could ‘curve’ a little bit, we would get a great fit.

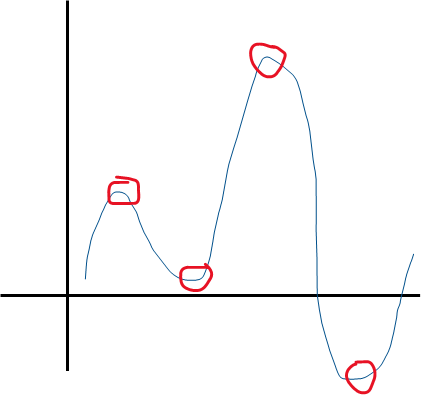

13.4.1 A Layman’s take on ‘Power Series Approximations’

Power series approximation allows you to express any function of \(x\) as a summation of terms with increasing powers of \(x\). Therefore any function can be approximated as:

Zero-th order estimation: \(g_0 (x) = a\)

First order estimation: \(g_1 (x) = a+bx\)

Second order estimation: \(g_2 (x) = a+bx+c x^2\)

Third order estimation: \(g_3 (x) = a+bx+c x^2+dx^3\)

And so on. Whatever is the maximum power of x in a function, it is that ‘order’ of approximation. All you have to do is to find the values of the constants \(a\), \(b\), \(c\) and \(d\) in order to get the function.

image.png

The number of ‘U-turns’ in a function’s graph plus 1 tell us the power of \(x\) in the function.

So the function above can be approximated by a 4 + 1 = 5th order function.

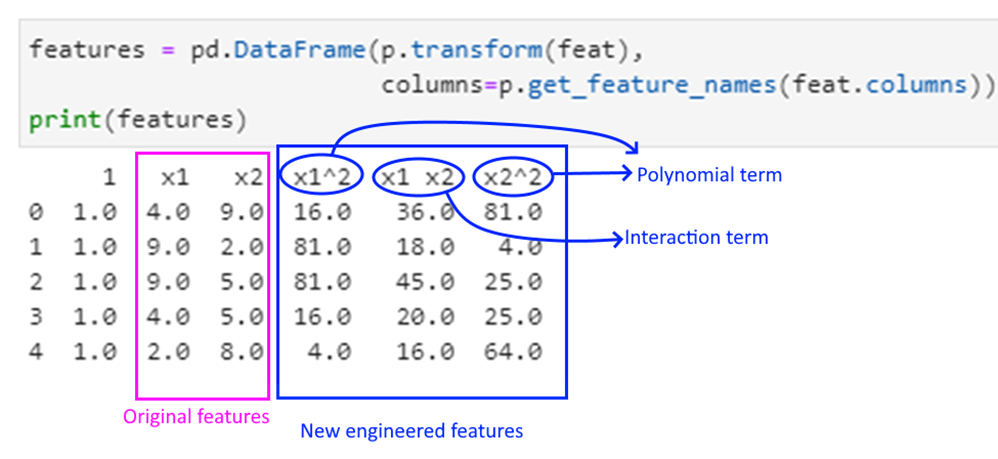

13.4.2 Polynomial Features Example

Polynomial regression is just OLS regression, but with polynomial features added to our \(X\) predictors. And we do that manually!! Let us see how.

We first need to ‘fit’ polynomial features to data which in our case is \(X\), and store this ‘fit’ in a variable we call, say \(p_X\). We can then transform any input to the polynomial feature set using transform().

Throughout our modeling journey, we will often see a difference between the fit and the transform methods. fit creates the mechanism, transform implements it. Sometimes these operations are combined in a single step using fit_transform(). What we do depends upon our use case.

The PolynomialFeatures function automatically inserts a constant, so if we use our \(X\) as an input, we will get the constant term twice (as we had added a constant earlier using add_constant). So we will use features instead of \(X\).

Polynomial features are powers of input features, eg for a feature vector \(x\), these could be \(x^2\),\(x^3\) etc.

Interaction features are products of independent features. For example, if \(x_1\),\(x_2\) are features, then \(x_1 \cdot x_2\) would be an example of an interaction feature.

Interaction features are useful in the case of linear models – and often used in regression. Let us move to the example.

We create a random dataframe, and try to see what the polynomial and interaction features would be.

Code

# Explaining polynomial features with a random examplefrom sklearn.preprocessing import PolynomialFeaturesimport pandas as pdimport numpy as npdata = pd.DataFrame.from_dict({'x1': np.random.randint(low=1, high=10, size=5),'x2': np.random.randint(low=1, high=10, size=5),'y': np.random.randint(low=1, high=10, size=5)})print('Dataset is:\n', data)feat = data.iloc[:,:2].copy()p = PolynomialFeatures(degree=2, interaction_only=False).fit(feat)print('\nPolynomial and Interaction Feature names are:\n', p.get_feature_names_out(feat.columns))

As mentioned earlier, polynomial regression is a form of regression analysis in which the relationship between the predictors (\(X\)) and the target variable (\(y\)) is modelled as an n-th degree polynomial in \(x\).

Polynomial regression allows us to fit a nonlinear relationship between \(X\) and \(y\).

So if we have \(x_1\) and \(x_2\) are the two predictors for \(y\), the 2nd order polynomial regression equation would look as follows:

\(y = a + b_1*x_1+b_2*x_2+ b_3*x_12+ b_4*x_22+ b_5*x_1*x_2+ \epsilon\)

The product terms towards the end are called the ‘interaction terms’.

Here is how to approach polynomial regression:

1. Decide the ‘order’ of the regression.

2. Generate the polynomial features (unfortunately Python will not do it for us, though R has a feature to just specify the polynomial order).

3. Perform a regression in a regular way, and evaluate the model.

4. Perform predictions.

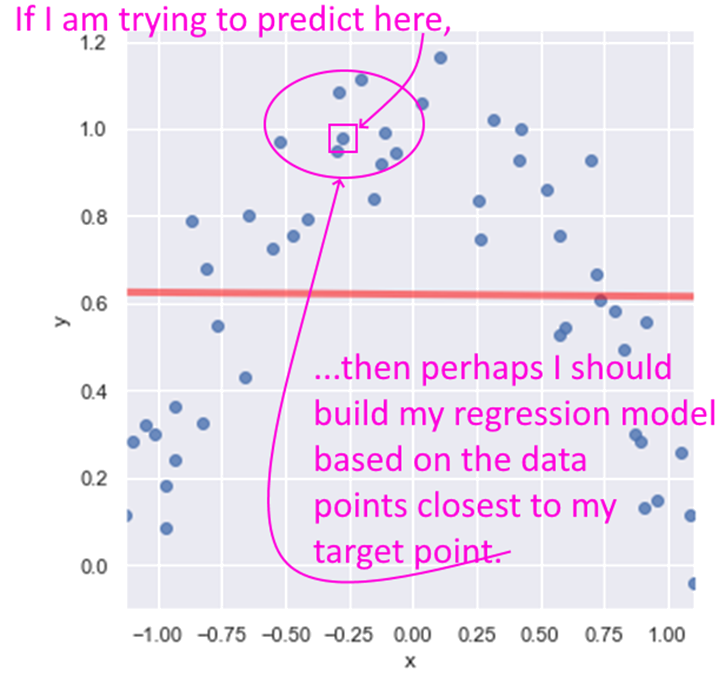

13.5 LOESS Regression

LOESS stands for Locally Weighted Linear Regression. The idea behind LOESS is very similar to the idea behind k-nearest neighbors. LOESS is a non-parametric regression method that focuses on data points closest to the one being predicted.

A key decision then is how many points closest to the target to include in the regression. Another decision is if any weighting be used to give greater weight to the points closest to the target. Yet another decision is to whether use simple linear regression, or quadratic, etc.

image.png

That The statsmodels implementation of LOESS does not allow the predict method. If you need to implement predictions using LOESS, you may need to use R or another tool. Besides, the LOESS model is very similar to the k-nearest neighbors algorithm which we will cover later.is all we will cover on LOESS.

13.6 Logistic Regression

Logistic Regression is about class membership probability estimation. What that means is that it is a categorization tool, and returns probabilities. You do not use logistic regression for predicting continuous variables.

Classes are categories, and logistic regression helps us get estimates of an observation belonging to a particular class (spam/not-spam, will-respond/will-not-respond, etc). We use the same framework as for linear models, but change the objective function as to get estimates of class probabilities.

One might ask: why can’t we use normal linear regression for estimating class probabilities?

The reason for that is that normal regression gives us results that are unbounded, whereas we need to bound probabilities to be between 0 and 1. In other words, because \(f(x) = \beta_0 + \beta_0 x_1 + \beta_0 x_2 + ... + \epsilon\), \(f(x)\) is unbounded and can go from \(-\infty\) to \(+\infty\), while we need probability estimates to be between 0 and 1.

How logistic regression solves this problem?

In order to address this problem (that normal regression gives us results that are not compatible with probabilities), we apply some mathematical transformations as follows:

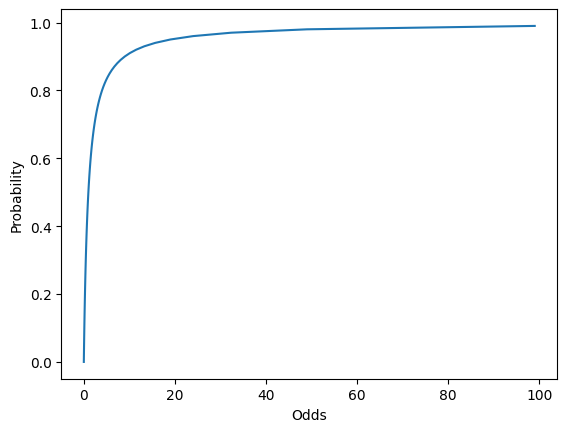

Instead of trying to predict probabilities, we can try to predict ‘odds’ instead, and work out the probability from the odds.

Odds are the ratio of the probabilities of an event happening vs not happening. For example, a probability of 0.5 equates to the odds of 1, a probability of 0.25 equates to odds of 0.33 etc. \(Odds = p/(1-p)\)

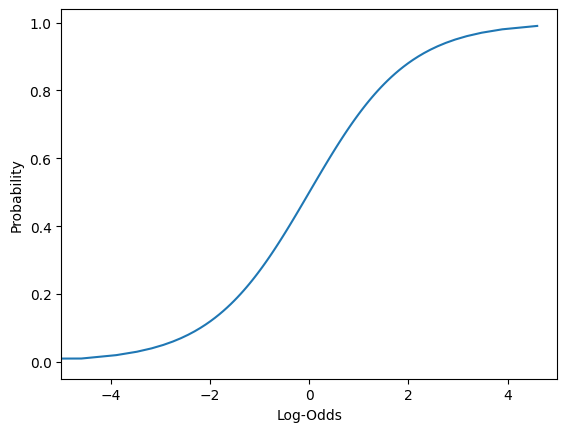

But odds vary from 0 to \(\infty\), which doesn’t help us.

However, if we take the log of the odds (log-odds), we get numbers that are between \(-\infty\) to \(+\infty\). We can now build a regression model to predict these log-odds.

These are the log-odds we get \(f(x)\) in our regression model to represent.

Then we can work backwards to calculate the probability.

Read the above again if it doesn’t register in one go!

Interpreting logistic regression results

What do probability estimates mean, when training data is always either 0 or 1?

If a probability of say, 0.2, is identified by the model, it means that if you take 100 items that have their class membership probability estimated to be 0.2 then about 20 will actually belong to the class.

13.6.1 Load the data

We use a public domain dataset where we need to classify individuals as being with or without diabetes. (Source: https://www.kaggle.com/uciml/pima-indians-diabetes-database)

This dataset is originally from the National Institute of Diabetes and Digestive and Kidney Diseases. The objective of the dataset is to diagnostically predict whether or not a patient has diabetes, based on certain diagnostic measurements included in the dataset. The target variable is a category, tagged as 1 or 0 in the dataset.

To approach this problem in a structured way, we will perform the following steps:

Step 1: Load the data, do some EDA

Step 2: Prepare the data, and split into train-test sets

Step 3: Fit the model

Step 4: Evaluate the model

Step 5: Use for predictions

13.6.3 Review the data

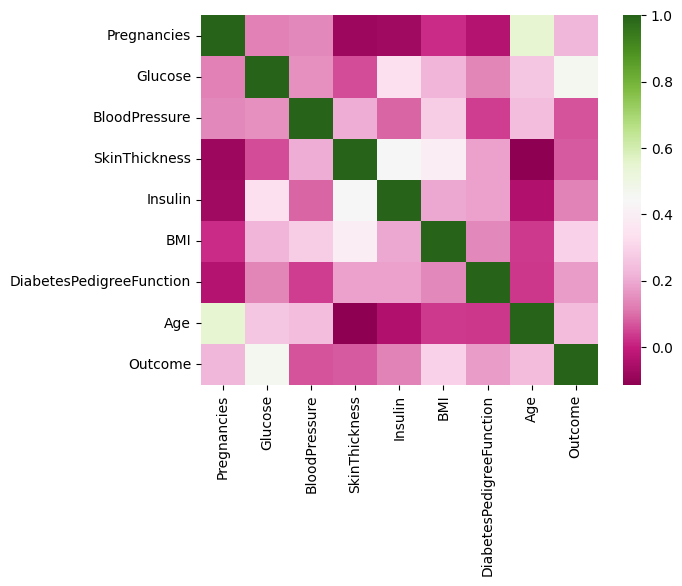

Lete us load the data, and do some initial exploration. The last column Outcome is our target variable, and the rest are features.

Code

df

Pregnancies

Glucose

BloodPressure

SkinThickness

Insulin

BMI

DiabetesPedigreeFunction

Age

Outcome

0

6

148

72

35

0

33.6

0.627

50

1

1

1

85

66

29

0

26.6

0.351

31

0

2

8

183

64

0

0

23.3

0.672

32

1

3

1

89

66

23

94

28.1

0.167

21

0

4

0

137

40

35

168

43.1

2.288

33

1

...

...

...

...

...

...

...

...

...

...

763

10

101

76

48

180

32.9

0.171

63

0

764

2

122

70

27

0

36.8

0.340

27

0

765

5

121

72

23

112

26.2

0.245

30

0

766

1

126

60

0

0

30.1

0.349

47

1

767

1

93

70

31

0

30.4

0.315

23

0

768 rows × 9 columns

Code

df.Outcome.value_counts()

Outcome

0 500

1 268

Name: count, dtype: int64

Code

df.describe()

Pregnancies

Glucose

BloodPressure

SkinThickness

Insulin

BMI

DiabetesPedigreeFunction

Age

Outcome

count

768.000000

768.000000

768.000000

768.000000

768.000000

768.000000

768.000000

768.000000

768.000000

mean

3.845052

120.894531

69.105469

20.536458

79.799479

31.992578

0.471876

33.240885

0.348958

std

3.369578

31.972618

19.355807

15.952218

115.244002

7.884160

0.331329

11.760232

0.476951

min

0.000000

0.000000

0.000000

0.000000

0.000000

0.000000

0.078000

21.000000

0.000000

25%

1.000000

99.000000

62.000000

0.000000

0.000000

27.300000

0.243750

24.000000

0.000000

50%

3.000000

117.000000

72.000000

23.000000

30.500000

32.000000

0.372500

29.000000

0.000000

75%

6.000000

140.250000

80.000000

32.000000

127.250000

36.600000

0.626250

41.000000

1.000000

max

17.000000

199.000000

122.000000

99.000000

846.000000

67.100000

2.420000

81.000000

1.000000

What we see: We notice that the mean of the different features appear to be on different scales. We also see that correlations are generally not high, which is a good thing.

13.6.4 Prepare the data, and perform a train-test split

We standardize the data (because we saw the features to have different scales, or magnitudes). Then we split it 75:25 into train and test sets.

Code

# Columns 0 to 8 are our predictors, or featuresX = df.iloc[:,:8]# Add the intercept term/constantX = sm.add_constant(X)# The last column is our y variable, the targety = df.Outcome# Now we are ready to do the train-test split 75-25, with random_state=1X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.25, random_state=1)

13.6.5 Create a model using the Statsmodels library

Fitting the model is a one line task with Statsmodels, with a call to the function.

Code

model = sm.Logit(y_train, X_train).fit()model.summary()

Optimization terminated successfully.

Current function value: 0.474074

Iterations 6

Logit Regression Results

Dep. Variable:

Outcome

No. Observations:

576

Model:

Logit

Df Residuals:

567

Method:

MLE

Df Model:

8

Date:

Sat, 02 Mar 2024

Pseudo R-squ.:

0.2646

Time:

11:28:58

Log-Likelihood:

-273.07

converged:

True

LL-Null:

-371.29

Covariance Type:

nonrobust

LLR p-value:

3.567e-38

coef

std err

z

P>|z|

[0.025

0.975]

const

-8.1521

0.810

-10.068

0.000

-9.739

-6.565

Pregnancies

0.1181

0.037

3.230

0.001

0.046

0.190

Glucose

0.0354

0.004

8.191

0.000

0.027

0.044

BloodPressure

-0.0146

0.006

-2.543

0.011

-0.026

-0.003

SkinThickness

-0.0027

0.008

-0.336

0.737

-0.019

0.013

Insulin

-0.0007

0.001

-0.658

0.510

-0.003

0.001

BMI

0.0915

0.018

5.214

0.000

0.057

0.126

DiabetesPedigreeFunction

0.5957

0.334

1.781

0.075

-0.060

1.251

Age

0.0138

0.011

1.286

0.198

-0.007

0.035

13.6.6 Run the model on the test set, and build a confusion matrix

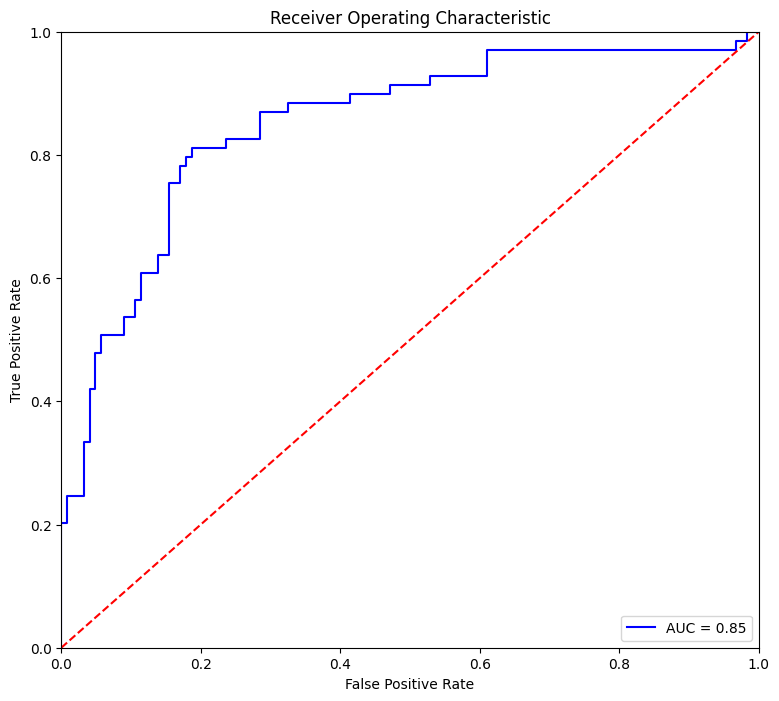

Review the model summary above. How is it different from the regression summary we examined earlier? How do we know the model is doing its job?

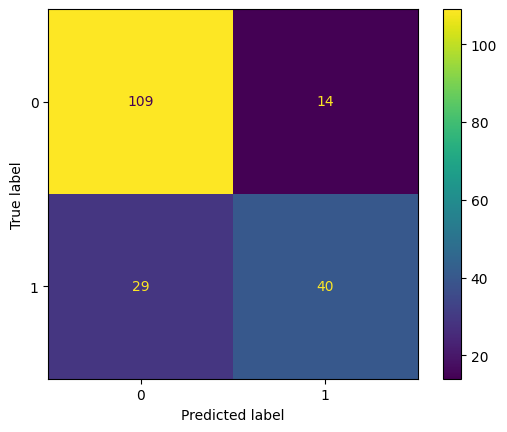

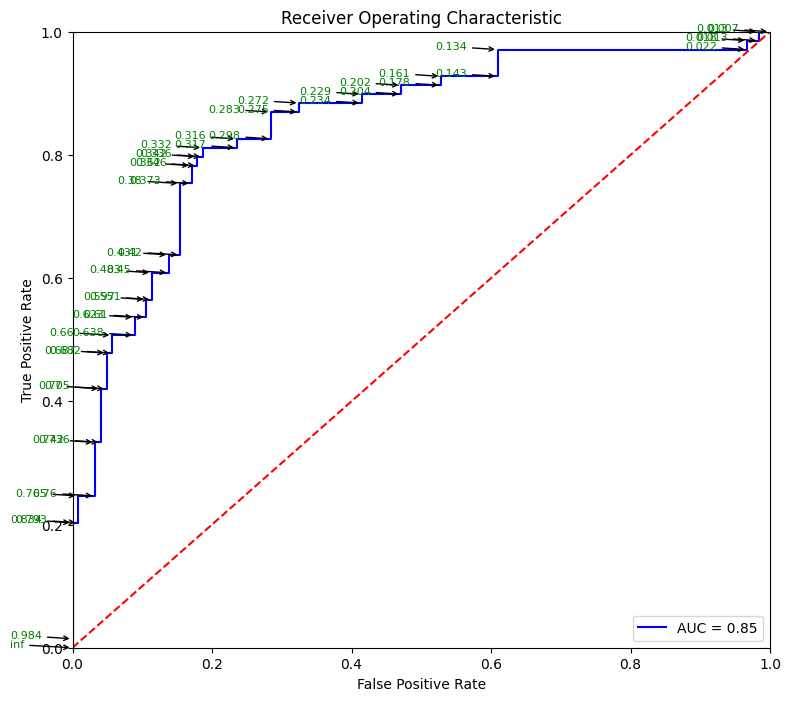

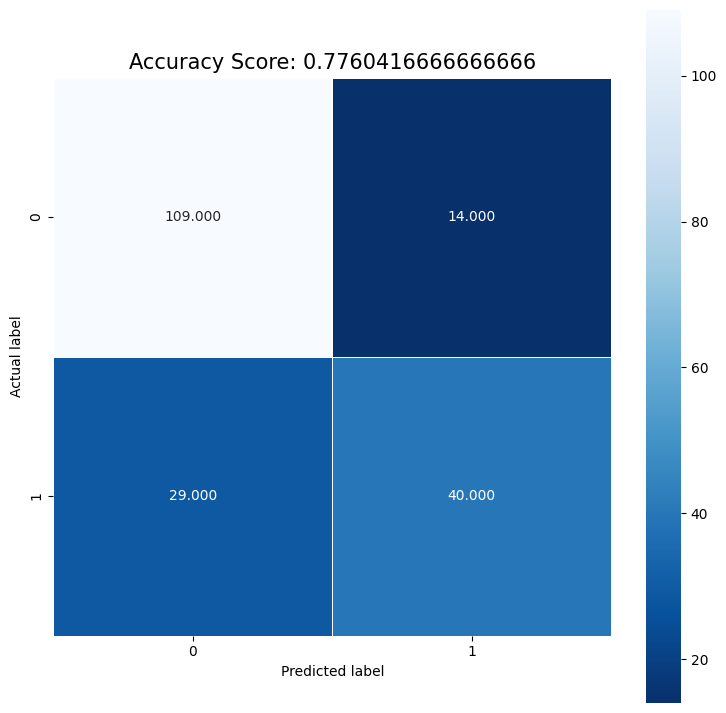

Next, we evaluate the model by studying the confusion matrix and the classification report. Below, we use a threshold of 0.50 to classify disease as 1 or 0. By moving this threshold around, you can control the instance of false positives and false negatives.

Probability Calibration. Logistic regression outputs well-calibrated probabilities (a predicted 70% means the event happens about 70% of the time). Many other classifiers (Random Forests, Gradient Boosting, SVMs) are not well-calibrated by default. Check calibration visually and correct it if needed:

from sklearn.calibration import CalibrationDisplay, CalibratedClassifierCV# Visualize calibrationCalibrationDisplay.from_estimator(model, X_test, y_test, n_bins=10)# Recalibrate a poorly calibrated model (e.g., GradientBoosting)calibrated_model = CalibratedClassifierCV(model, method="isotonic", cv=5)calibrated_model.fit(X_train, y_train)

Calibration is critical when the predicted probability will be used to make business decisions (e.g., ranking customers by churn risk).

Code

# Create predictions. Note that predictions give us probabilities, not classes!pred_prob = model.predict(X_test)# Set threshold for identifying class 1threshold =0.50# Convert probabilities to 1s and 0s based on thresholdpred = (pred_prob>threshold).astype(int)# confusion matrixcm = confusion_matrix(y_test, pred)print ("Confusion Matrix : \n", cm)# accuracy score of the modelprint('Test accuracy = ', accuracy_score(y_test, pred))

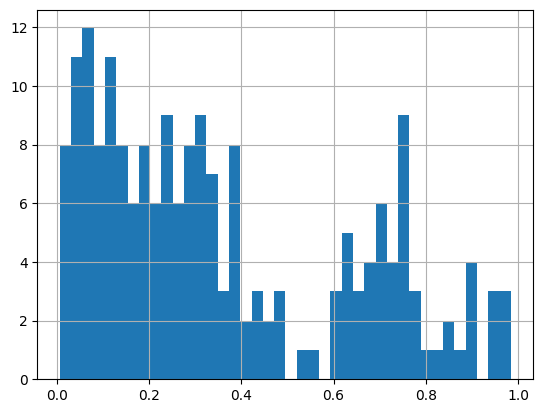

# A histogram of probabilities. Why not?pred_prob.hist(bins=40)

13.6.7 Predict a new case

Next time when a new patient comes in, you can predict with 77.6% accuracy the incidence of disease based on other things you know about them.

Use model.predict(X), where \(X\) is the vector of the attributes of the new patient.

Remember to scale \(X\) first using the preprocessing step of standardization by using the same scaler we had set up earlier (as to use the same \(\mu\) and \(\sigma\))!

We get a probability estimate of about 5.6%, which we can evaluate based on our threshold.

Code

# let us see what our original data looks likedf.sample(1)

Pregnancies

Glucose

BloodPressure

SkinThickness

Insulin

BMI

DiabetesPedigreeFunction

Age

Outcome

432

1

80

74

11

60

30.0

0.527

22

0

Code

# Also let us see what our model consumesX_test.sample(1)

const

Pregnancies

Glucose

BloodPressure

SkinThickness

Insulin

BMI

DiabetesPedigreeFunction

Age

277

1.0

0

104

64

23

116

27.8

0.454

23

Code

# Let us now create a dataframe with a new case with imaginary valuesnew_case = pd.DataFrame({'Pregnancies': [1],'Glucose':[100],'BloodPressure': [110],'SkinThickness': [40],'Insulin': [145],'BMI': [25],'DiabetesPedigreeFunction': [0.8],'Age': [52]})new_case

Pregnancies

Glucose

BloodPressure

SkinThickness

Insulin

BMI

DiabetesPedigreeFunction

Age

0

1

100

110

40

145

25

0.8

52

Code

# Our new data on which to predict looks like this: new_case = np.array(new_case).squeeze()new_case = np.insert(new_case,0, 1)new_case

13.6.9 EXTRA - Create model using the sklearn library

Code

# For running this, you need to convert all column names to be strings firstX_train.columns = [str(p) for p in X_train.columns]X_test.columns = [str(p) for p in X_test.columns]

Code

from sklearn.linear_model import LogisticRegressionlogisticRegr = LogisticRegression()logisticRegr.fit(X_train, y_train)predictions = logisticRegr.predict(X_test)# Use score method to get accuracy of modelscore = logisticRegr.score(X_test, y_test)print(score)

# Plotting Probability vs Oddsimport seaborn as snsimport matplotlib.pyplot as pltdf = pd.DataFrame({'Probability': np.arange(0,1, 0.01), \'Odds':np.arange(0,1., 0.01) /\ (1-np.arange(0,1., 0.01)) })sns.lineplot(data = df, x ='Odds', y ='Probability');

Code

# Plotting log-odds# We add a very tiny number, 1e-15 (10 to the power -15) to avoid the divide by zero error for the log functionplt.xlim(-5,5)sns.lineplot(data = df, x = np.log(df['Odds'] +1e-15), y ='Probability',)plt.xlabel("Log-Odds");

Regression Discussion Ends here

*** ## Generating correlated variables

Code

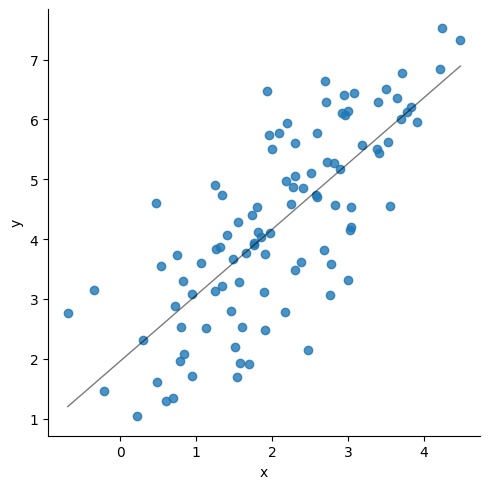

### Generating correlated variables### Specify the mean of the two variables (mean),### Then the correlation between them (corr),### and finally, the standard deviation of each of them (stdev).### Also specify the number of observations needed (size).### Update the below three linesmean = np.array([2,4])corr = np.array([.75])stdev = np.array([1, 1.5])size =100### Generate the numberscov = np.prod(stdev)*corrcov_matrix = np.array([[stdev[0]**2, cov[0]], [cov[0], stdev[1]**2]], dtype ='float')df = np.random.multivariate_normal(mean= mean, cov=cov_matrix, size=size)df = pd.DataFrame(df, columns = ['x', 'y'])# sns.scatterplot(data=df, x = df.iloc[:,0], y=df.iloc[:,1])sns.lmplot(data=df, x ="x", y="y", line_kws={"lw":1,"alpha": .5, "color":"black"}, ci=1)print('Correlation matrix\n',df.corr())print(df.describe())print('\n', stats.linregress(x = df['x'], y = df['y']))

Correlation matrix

x y

x 1.000000 0.761016

y 0.761016 1.000000

x y

count 100.000000 100.000000

mean 2.089719 4.261462

std 1.087460 1.574654

min -0.687144 1.038394

25% 1.341127 3.127999

50% 2.046680 4.176002

75% 2.904254 5.583037

max 4.476411 7.521391

LinregressResult(slope=1.1019603629813395, intercept=1.9586752461394572, rvalue=0.7610163850816325, pvalue=4.010217987867538e-20, stderr=0.09489092704985068, intercept_stderr=0.22329966742161625)

Code

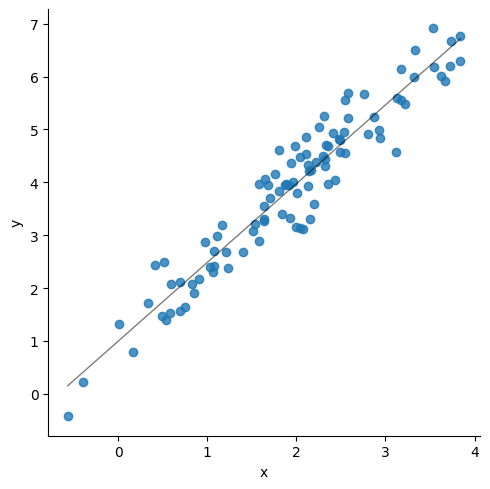

### Update the below three linesmean = np.array([2,4])corr = np.array([.95])stdev = np.array([1, 1.5])size =100### Generate the numberscov = np.prod(stdev)*corrcov_matrix = np.array([[stdev[0]**2, cov[0]], [cov[0], stdev[1]**2]], dtype ='float')df = np.random.multivariate_normal(mean= mean, cov=cov_matrix, size=size)df = pd.DataFrame(df, columns = ['x', 'y'])# sns.scatterplot(data=df, x = df.iloc[:,0], y=df.iloc[:,1])sns.lmplot(data=df, x ="x", y="y", line_kws={"lw":1,"alpha": .5, "color":"black"},ci=1)print('Correlation matrix\n',df.corr())print(df.describe())print('\n', stats.linregress(x = df['x'], y = df['y']))

Correlation matrix

x y

x 1.000000 0.956126

y 0.956126 1.000000

x y

count 100.000000 100.000000

mean 1.949915 3.899637

std 0.975078 1.519397

min -0.565047 -0.426430

25% 1.225198 2.888537

50% 2.024962 3.994811

75% 2.503927 4.868860

max 3.840545 6.911640

LinregressResult(slope=1.4898649159820154, intercept=0.9945266231874772, rvalue=0.9561256680834156, pvalue=4.6887116999071444e-54, stderr=0.04611290814962349, intercept_stderr=0.10043132061014937)